Page 77 - EINF2022

P. 77

NON-FINANCIAL INFORMATION STATEMENT

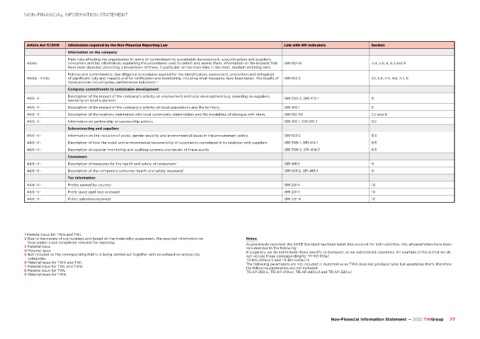

Article Act 11/2018 Information required by the Non-Financial Reporting Law Link with GRI indicators Section

Information on the company

Main risks affecting the organisation in terms of commitment to sustainable development, subcontractors and suppliers,

44.6d consumers and tax information, explaining the procedures used to detect and assess them. Information on the impacts that GRI 102-15 4.4, 4.6, 6, 8.3 and 9

have been detected, providing a breakdown of these, in particular on the main risks in the short, medium and long term.

Policies and commitments. due diligence procedures applied for the identification, assessment, prevention and mitigation

44.6b - 44.6c of significant risks and impacts and for verification and monitoring, including what measures have been taken. The results of GRI 103-2 3.1, 3.4, 4.4, 4.6, 4.7, 6

those policies including key performance indicators .[7]

Company commitments to sustainable development

Description of the impact of the company's activity on employment and local development (e.g. spending on suppliers,

44.6 -V- GRI 203-2, GRI 413-1 8

spending on local suppliers).

44.6 -V- Description of the impact of the company's activity on local populations and the territory. GRI 413-1 8

44.6 -V- Description of the relations maintained with local community stakeholders and the modalities of dialogue with them. GRI 102-43 2.2 and 8

44.6 -V- Information on partnership or sponsorship actions GRI 413-1, GRI 201-1 8.2

Subcontracting and suppliers

44.6 -V- Information on the inclusion of social, gender equality and environmental issues in the procurement policy. GRI 103-2 8.3

44.6 -V- Description of how the social and environmental responsibility of suppliers is considered in its relations with suppliers GRI 308-1, GRI 414-1 8.3

44.6 -V- Description of supplier monitoring and auditing systems and results of these audits GRI 308-2, GRI 414-2 8.3

Consumers

44.6 -V- Description of measures for the health and safety of consumers 8 GRI 416-1 9

44.6 -V- Description of the company’s consumer health and safety measures 9 GRI 103-2, GRI 418-1 9

Tax information

44.6 -V- Profits earned by country GRI 201-1 10

44.6 -V- Profit taxes paid (not accrued) GRI 201-1 10

44.6 -V- Public subsidies received GRI 201-4 10

1 Material issue for TWG and TWL

2 Due to the nature of our business and based on the materiality assessment, the required information on Notes:

food waste is not considered relevant for reporting. As previously reported, the SASB Standard has been taken into account for both activities. Not all parameters have been

3 Material issue included due to the following:

4 Material issue In Logistics, we do not include those specific to transport, as we subcontract operators. An example of this is that we do

5 Not included as the corresponding Matrix is being carried out together with an exhaustive analysis by not include those corresponding to TR-RO-120a.1

categories. TR-RO-320a.1/3 and TR-RO-540a.1/3

6 Material issue for TWA and TWL The following parameters are not included in Automotive as TWA does not produce tyres but assembles them, therefore

7 Material issue for TWL and TWA the following parameters are not included:

8 Material issue for TWL TR-AP-250.a., TR-AP-410-a1, TR-AP-440.a.1 and TR-AP-520.a.1

9 Material issue for TWA

Non-Financial Information Statement — 2022 TWGroup 77